Developed by Michael Meese, PhD, FLMI, BG (U.S. Army, retired). For questions or comments, email [email protected].

Why did the Nation adopt a New “Blended” Retirement System?

The previous “defined benefit” retirement system was good and generous, but only provided benefits at the time of a servicemember’s retirement, which was normally at 20 years. Over 83 percent of all servicemembers “will never benefit from a traditional 20-year Uniformed Service retirement.”[i] After years of study and proposals, Congress approved the changes to the retirement system in the 2016 National Defense Authorization Act.

Who is covered by the New Retirement System? Who is not covered? Who has a choice?

It depends on your Date of Initial Entry into Military Service (DIEMS) and your Pay Entry Basic Date (PEBD), both of which are on Leave and Earning Statement (LES).

· DIEMS on or after 1 January 2018—you are in the new blended retirement system.

· PEBD on or before 31 December 2005—You will are in the old system

· 2006 through 2017—If your PEBD or DIEMS is between 2006 and 2017 (i.e. you have less than 12 years of service), you have a choice of staying in the old “defined benefit” system or opting into the new “blended” system.

How does the choice work for reservists?

It is similar for reservists, except that instead of 12 years, you are eligible to “opt in” to the new blended retirement system if you have less than 4320 retirement points.

Why do they call it a “Blended” Retirement System (BRS)?

The new military retirement system is a “blend” of defined contributions, defined benefits, and a continuation bonus:

· First, it adds a “defined contribution” component, similar to a 401k in the private sector. It starts with an automatic contribution by the military of 1 percent of a servicemember’s base pay in their personal Thrift Savings Plan account. The servicemember can also contribute a percentage of his or her base pay, which the military will match up to 5 percent. After serving two years, soldiers, Marines, sailors, airmen, and Coast Guardsmen can take those savings, with the matching contribution, to their next job.

· Second, to retain experienced officers and noncommissioned officers, the new plan provides a mid-career continuation pay “bonus” at 12 years of service of at least 2.5 months of pay for those who commit to serve an additional 4 years.

· Third, the new plan retains, but reduces by 20 percent, the “defined benefit” pension paid to retirees after 20 years of service.

Is the new system more generous or less generous?

The new military retirement system is unequivocally more generous for anyone who does not stay until retirement. Calculations by the Military Compensation and Retirement Modernization Commission (MCRMC) explain that if a servicemember stayed until retirement and successfully invested their own funds, the matching funds, and continuation bonuses, in the TSP and received historically average returns from the TSP, then they could be at least as well off as if they were under the previous system.[ii] Overall the MCRMC estimated that the new system would result “in annual steady-state savings of $1.9 billion.”[iii]

If my DIEMS date is in 2006 to 2017, should I opt into the new system?

This is a difficult and personal question that each person must answer for themselves. The military will have substantial training to help you understand your options and decide. It really comes down to your answer to two challenging questions:

(1) Do you plan to retire from the military? Are you: “Staying” “Leaving” or “Unsure”?

(2) Will you save the 5% to get matching 5% into TSP? “Yes” or “No”

· If definitely “Staying,” à old system is likely better.

· If definitely “Leaving,” and “Yes” will save 5% à new system is better.

· If you are “Unsure,” and “No” you won’t save 5%, à old system is likely better, but only pays if you stay until 20 years of service. The 1% automatic contribution will likely not make up for the 20% reduction in retirement income, if you do stay.

· If you are “Unsure,” and “Yes,” you would save 5% to get a full 5% matching, this is the most difficult situation. You really need to evaluate your probability of staying until retirement to determine which option is financially better for you. The biggest downside would be if you opted for the old system and then left the service. You will still take the 5% you are saving in the TSP with you, but will have forgone the 5% matching. The downside of opting into the new system and then staying in the Army is that your eventual retirement would not be as generous, but you would have the advantage the 5% match throughout the remainder of your career. And retiring at 20 years with a pension of 40% of your salary for life is still very generous. So although the decision may be difficult, it is between two pretty good options.

I am a cadet or midshipman, do I have the option of staying in the old system?

Yes. If you check your DIEMS date on your Leave and Earning Statement (LES), it should reflect that anyone from before the class of 2022 entered active service with DIEMS before 1 January 2018 and so will have a choice of systems. Similarly, a cadet enrolled in the Senior Reserve Officer Training Corps, who has signed an agreement to serve as a commissioned officer in a Uniformed Service upon graduation and receives basic pay or inactive duty pay, will also have a choice of which retirement system to opt into.[iv]

When do I have to decide?

You have until 31 December 2018 to “opt in” to the new blended retirement system. DoD and each of the military services will be doing training and explain to soldiers, sailors, airmen, and marines what their options are. No one will be forced into making a decision to go into the new system and if you do not make a decision, you will stay grandfathered in the old defined benefit system.

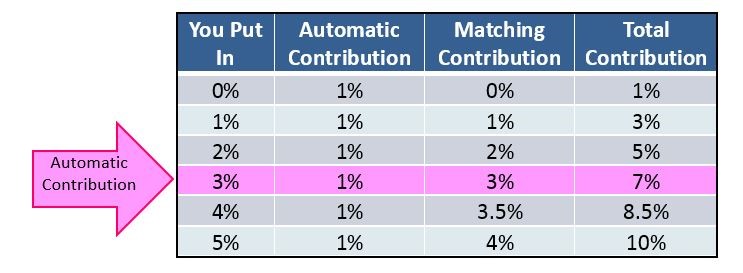

How does the “defined contribution” matching work?

In the new “blended” plan, the government provides the 1% “free” contribution after 60 days of service. For those “opting in” to the new system, the 1% “free” contribution will begin immediately. The government will also “automatically” enroll all service members at the 3% personal contribution level after 60 days of service or in the month after they “opt in” to the new system. After 24 months of service for new service members or immediately after the election for those who have “opted in” to the new blended retirement system, the government will match the member’s contribution according to the main image associated with this article.

You can always change your contribution from the automatic 3%. If you were to increase to 5%, then you will get additional matching contributions from the government totaling 5%. You can put more than 5% of your income into TSP, but a 5% contribution maximizes the government match. You can also decrease your contribution to 0% of your pay, and would still receive the 1% automatic contribution into your pay. Additionally, if you have elected 0% as your contribution level, each year the government will re-enroll you into TSP at the 3% automatic contribution level. You will then have to contact finance to change your contribution level.

Is the contribution a traditional “tax deferred” contribution or “Roth” contribution?

The contribution is treated, by default, as a “traditional” tax-deferred contribution, not Roth, unless you elect to designate all or part of your contribution as Roth (and then you would have to pay taxes on it in the year that the contribution is made).[v]

Where do the contributions go?

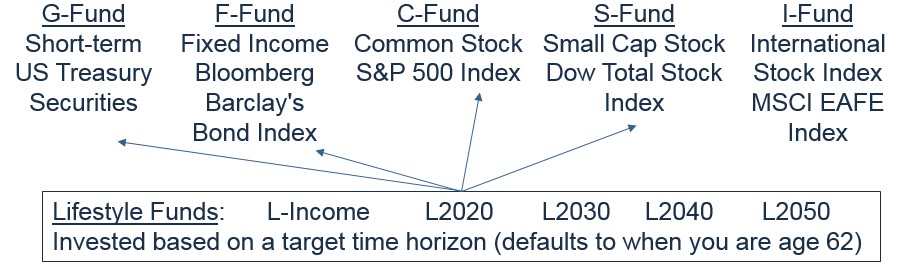

Contributions from you and the government are invested in the Thrift Savings Plan, which is a retirement savings and investment plan for Federal employees and military members to offer the same types of savings and tax benefits that many private corporations offer their employees under 401(k) plans. It has low administrative and investment fees and you have a choice of directing your investments into one of five “sector” funds listed below or into one of five “lifestyle” funds. The lifestyle funds use a combination of the sector funds to balance risk and return based on a targeted retirement date.

If you do not choose a fund, your contributions will go to the lifestyle fund that with a year that is closest to the date when you will turn age 62.

When do the contributions “vest”? When do I have access to the money?

Remember that all of the contributions—both yours and the governments—are part of a “qualified retirement plan,” which means that, in general, you cannot access the funds until you are 59½ without paying a penalty.

Current servicemembers who “opt in” to the new system are fully-vested immediately and can take their contributions and all matching contributions with them when they leave the service.

For those entering military service after 1 January 2018, the one-percent automatic contribution (which starts after 60 days) vests at two years. Funds that you contribute and any government matching funds are fully vested immediately and you can “take those with you” to a future job whenever you leave the service.

Bottom line: if you leave with less than two-years of service, you lose the automatic one-percent and will not have earned any matching contributions. Otherwise, you keep all contributions and they can transfer with you when you leave the service.

When do the government’s contributions ever stop?

The automatic and government contributions stop when you complete 26 years of service.

How does this work for reservists?

Remember that all of the contributions—both yours and the governments—are part of a “qualified retirement plan,” which means that, in general, you cannot access the funds until you are 59½ without paying a penalty.

How does the mid-career continuation pay “bonus” work?

If you are in the Blended Retirement System, then you are eligible for a one-time bonus payment that is paid between the 8th and 12th year of service. The bonus will be equal to at least 2½ times your monthly base pay and could be up to 13 times your monthly base pay. The service will adjust the size and timing of the bonus based on the needs of the service. To receive the continuation bonus, you must agree to serve an additional 3 years of service.

Are there changes in the payment of the “deferred benefit” (pension) at retirement?

The biggest change is that the retirement pension is reduced by 20% from 2½ % per year of service to 2% per year of service for each year of service. Under the blended retirement, at 20 years, you will receive 40% of your highest 36 months of base pay (instead of 50%). At 30 years, you will receive 60% of your highest 36 months of base pay (instead of 75%).

Additionally, under the new system, you can choose to receive an up-front “lump sum” accelerated payment of 25% or 50% of your retired pay in exchange for accepting reduced retired pay until until you reach full retirement age (normally age 67). This lump sum might be advantageous to buy a home, start a business, or pay for some other large expense immediately upon retirement. You should carefully examine the costs and benefits of such a lump sum payment before you accept it.

Where can I get more information?

Look at the AAFMAA Intel Center at: https://www.aafmaa.com/Newsroom/INTELCenter

Look at the DoD website: http://militarypay.defense.gov/BlendedRetirement/

Email Mike, the author of this article, and the COO of AAFMAA, at [email protected] with specific questions.

[i] Report of the Military Compensation and Retirement Modernization Commission, Final Report, January 2015, p. 3

[ii] See Report of the Military Compensation and Retirement Modernization Commission, Final Report, January 2015, pp. 33-34.

[iii] See Report of the Military Compensation and Retirement Modernization Commission, Final Report, January 2015, p. 255.

[iv] See Department of Defense, Memorandum, Subject: Implementation of the Blended Retirement System, 27 January 2017, Attachment 1, p. 6.

[v] See Department of Defense, Memorandum, Subject: Implementation of the Blended Retirement System, 27 January 2017, Attachment 1, p. 11.