.svg)

Wealth Builder Life Insurance

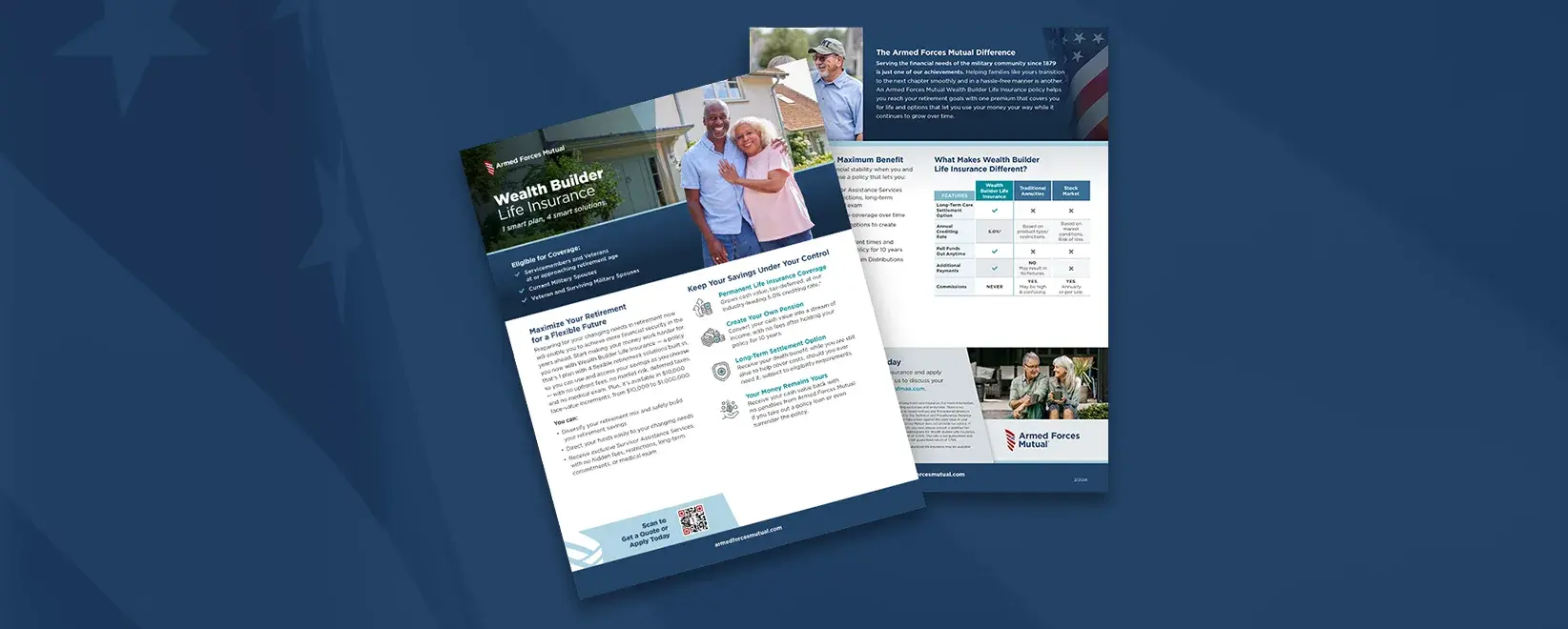

Make your retirement savings work harder with our industry-leading 5.0% crediting rate* while creating flexible options for your future — all with no upfront fees, no market risk, deferred taxes, and no medical exam. Policies are available in $10,000 face value increments from $10,000 to $1 million.

1 Plan, 4 Retirement Solutions

Wealth Builder Life Insurance gives you complete control over your retirement savings with multiple built-in options.

Your Savings, Your Control

Wealth Builder Life Insurance transforms your retirement savings into a versatile financial tool that can satisfy your changing needs in retirement.

Wealth Builder Life Insurance is designed for members of the military community, their spouses and widows/widowers, typically over age 55, who want to maximize their retirement savings while creating flexible options for the future.

Growth & Security

Income Options

Long-Term Care Settlement Option

Using Your Savings

Who Can Apply?

Wealth Builder Life Insurance is designed for members of the military community, their spouses and widows/widowers, typically over age 55, who want to maximize their retirement savings while creating flexible options for the future.

Retirement Planning

Valuable resources to help you maximize your retirement savings and create financial security.

Denotes content only available to subscribers

Denotes content only available to subscribers

Put Your Retirement Savings to Work

Join thousands of Veterans who have discovered how Wealth Builder can transform retirement savings into lifetime security with our industry-leading 5.0% crediting rate and no fees or commissions.